DECRYPTING PERSONAL LOAN INTEREST RATES AND HOW TO OBTAIN IDEAL INTEREST RATES

In the rapidly evolving digital world, online financial services are becoming increasingly convenient, allowing users to instantly apply for loans with simple actions on mobile devices or computers. Alongside the clear benefits that a portion of the population has already embraced, many still hesitate to choose online consumer loan products due to a lack of understanding about product information, interest rates, and loan terms. If you're also pondering, let's decrypt consumer loan interest rates together with Shinhan Finance in the article below!

What is a consumer loan interest rate?

Consumer loan interest rate is one of the most crucial factors that anyone considering borrowing needs to carefully consider. It is the percentage rate that borrowers must pay on top of the initial loan amount, usually calculated on an annual basis, and is the primary source of income for banks and financial institutions when providing lending services.

Interest rates can vary widely depending on various factors such as economic conditions, central bank policies, the borrower's credit profile, and the loan term. In the consumer lending market, there are two common types of interest rates: interest rates based on the outstanding balance and interest rates based on diminishing balance. Understanding interest rates helps borrowers to plan their finances more accurately and optimize their borrowing costs.

Common methods of calculating consumer loan interest rates

Currently, there are two common methods of calculating consumer loan interest rates that borrowers need to know to manage their loans effectively:

1. Interest rates based on the outstanding balance:

The method of calculating interest based on the outstanding balance is calculated based on the initial principal amount you borrow and does not decrease with the amount of principal repaid. This means that, even if you have repaid part of the principal, the monthly interest you have to pay is still based on the total initial loan amount. Here is how the monthly payment is calculated:

Monthly Interest = Outstanding Balance x Interest Rate / Loan Term (A)

Monthly Principal Payment = Outstanding Balance / Loan Term (B)

Monthly Payment = (A) + (B)

Example: A customer takes out a loan of 100 million VND with an annual interest rate of 10% and a loan term of 2 years, paying interest on the outstanding balance. Therefore, each month, the customer will need to pay an interest amount of 416,666.67 VND and a monthly principal amount of 4,166,667 VND for 24 months.

Note that this table only shows the monthly interest amount based on a simple formula and does not account for any other possible fees that may affect the actual monthly payment amount.

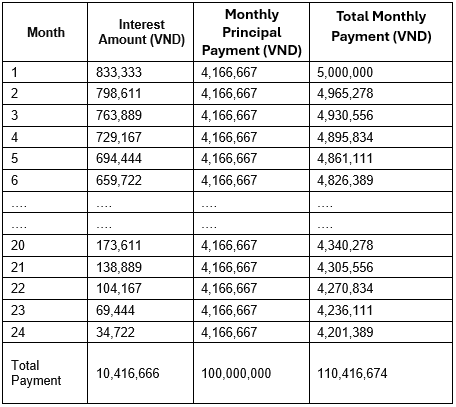

2. Interest rates based on diminishing balance:

The method of calculating interest based on diminishing balance focuses on applying interest rates to the remaining principal balance after each payment period. Here is the basic formula for this calculation:

Interest Amount = [total (actual balance x number of days maintaining the actual balance x interest rate for calculating interest)] / 365

Example: A customer takes out a loan of 100 million VND with an annual interest rate of 10% and a loan term of 2 years, repaying consumer loan interest based on diminishing balance. The amount the customer will have to pay per month is as follows:

The "secret" to obtaining ideal loan interest rates

When it comes to consumer loans, a good interest rate will save you a significant amount of money because interest affects the total interest amount you will pay over the loan term. Here are some tips to help you secure an ideal interest rate:

Improve your credit score: By making timely payments on existing loans and reducing your debt-to-income ratio, borrowers with high credit scores often receive lower interest rates.

Choose a suitable loan term: Consider choosing the appropriate loan term to also reduce interest costs. Short-term loans often have lower interest rates compared to long-term loans but require higher monthly payments.

Comparison: Compare interest rates from different banks and financial institutions, negotiate with financial service providers to find the best possible interest rate.

Consider early repayment capabilities: Consider the ability to make early payments, which can reduce the total interest costs you have to pay (additional early repayment fees need to be considered).

In summary, understanding online loan interest rates and common interest rate calculation methods is an important first step in effectively managing your consumer loan. By choosing the right financial institution, you not only optimize the interest rate but also ensure that your loan contributes to supporting your personal financial goals flexibly and sustainably.

If you are looking for a reputable place to apply for a loan with ideal interest rates, Shinhan Finance is the optimal financial support address, helping customers confidently apply for loans to serve their personal life needs. Loan products at Shinhan Finance offer attractive benefits including:

- Diverse loan packages tailored to customer needs such as car loans, home repairs, travel, education, or healthcare, etc.

- Competitive interest rates in the market.

- Fast procedures, maximum customer support from staff.

- Many preferential programs to help customers access loans easily and conveniently.

---------------------------------

The fastest channels to register for a loan:

- Hotline: 1900 54 54 49 (press 2 – Loan consultation)

- Website Shinhan Finance

- iShinhan financial management application

- Fanpage Shinhan Finance

- Directly at Shinhan Finance transaction counters: See the address details of Shinhan Finance branches.

Sincerely,

Shinhan Finance